November 18, 2018

Understanding the viability of bluechip funds can help you plan your investment and get a well-rounded portfolio.

Understanding the viability of bluechip funds can help you plan your investment and get a well-rounded portfolio.

It is a well-known fact that market-linked investments are subject to a certain degree of risk. However, certain equity funds offer higher growth prospects with the risk element evened out over the long term. One such fund is the Emerging blue chip fund, or blue chip funds in general.

What is a bluechip fund?

The term ‘bluechip’ comes from the game of poker, where the blue coloured chip is the most expensive or valuable of all. The same logic is applied to the bluechip fund – these are equity funds of large multinationals or companies with a long and well-established track record of high performance and market credibility. Companies offering blue chip funds are normally in the top 3 performance bracket in their sector or industry.

Given their reputation and economic standing, bluechip equity funds are those with a large market capitalisation, usually in crores of Rupees. They are normally listed on the stock exchange.

Investors earn via dividend payments from these funds. They are considered relatively ‘safe’ funds to invest in, with a higher propensity for stable and regular growth.

However…

- These equity funds offer dividend payouts since their prices normally do not move much. The dividends can become a valuable second income for investors.

- Having mentioned the risk factor, we would be remiss in not mentioning that the bluechip funds are amongst the highest performers among most equity funds, year on year. These funds have been seen to perform over the benchmark indexes set for them over the last decade.

- The size and composition of the company alone does not automatically guarantee that the bluechip fund is safe. Even the best in class bluechip equity funds like the Emerging Bluechip Fund carry a moderate amount of risk. But this is easily attributable to all equity funds. The key is to remain invested for a longer time frame to reap the rewards of the fund.

- They offer stability to your portfolio, with expert handling by the fund manager (but do partner with a reputed fund house when you buy the fund). The fund can normally recover itself in a bearish market, or when there is a downturn for some reason. This is because the fund can ride market volatility much better.

- Investors have the option of investing in blue chip funds, blue chip ULIPs, etc. This is because the fund moves in the broader market only.

- They are more expensive. This factor might deter new investors from seeking investment in blue chip equity funds, however, they are a viable option for their growth potential. Yet, it is not ideal to have too many bluechip funds in your portfolio, and you can diversify with a range of mid-cap and small-cap funds.

Tags:

budgeting,

Cash Flow,

economy,

financial planning,

Funds,

investments,

money

February 12, 2018

The money market will provide you with investment instruments like ULIPs that come with a fair combination of investment and life coverage at once. The premium that you pay for ULIPs are segregated into 2 parts; one portion goes towards investment instruments present in the money market, while the other one goes towards meeting your risk coverage on life. There are a few inherent benefits attached to ULIPs.

The money market will provide you with investment instruments like ULIPs that come with a fair combination of investment and life coverage at once. The premium that you pay for ULIPs are segregated into 2 parts; one portion goes towards investment instruments present in the money market, while the other one goes towards meeting your risk coverage on life. There are a few inherent benefits attached to ULIPs.

5 key advantages of ULIPs over all conventional life insurance policies:

Identify the right blend of investment

Picking the market entities in the right blend often depends on your investment risk appetite. For those of you that are low-risk takers, investing in debt funds is a good ploy. Likewise the moderate risk-takers can invest in balanced funds, while the high-risk bearers can think of equity funds. Balanced funds are a good option lying between equity funds and debt funds. You’ll be able to switch funds once you gain considerable market outlook.

Investment Flexibility

With an ULIP, you’ll gain the right to invest your entire premium value besides gaining opportunities to allocate additional amounts on the policy. Other investment plans don’t yield so much of flexibility. Depending on your risk appetite and your financial profile, you may choose between these two investment strategies:

Life-Stage Strategy: The years remaining towards your policy maturity and your age help in asset allocation.

Self-Managed Strategy: Your fund choice helps in allocating your money. This option safeguards the financial future of your child even when you aren’t there.

Long term investment

ULIPs prove to be a great option for fulfilling long-term investment goals e.g. launching a start-up, buying your new car, and buying a property. ULIPs are designed to yield more returns and that too for a longer duration; they owe this power to their compounding nature. Even if you decide on quitting the ULIP policies after a period of 5 years, you’ll be amazed to see how much more you’ve saved than what you’d see with other investment options. Your money will grow with a much greater momentum and for a longer duration than how you usually see it grow in your savings bank or with your fixed deposits. All you need to do is to determine the amount of investment with the help of an online premium calculator.

Life coverage

Life insurance companies are only known to offer ULIPs in the form of a product. Besides yielding financial protection, ULIPs are known to fulfill your investment needs. Compared to a term plan, the life cover attached to ULIPs may be smaller but they do come with life cover. When it comes to fulfilling your financial goals in the long run, ULIPs constitute a strong investment opportunity. Prior to investing in ULIPs, you must check out the performance of all individual funds in great details. This is likely to provide more insight into investment options with quality returns.

Tax Rebates

Tax benefits aren’t always attached to investment option that you come across in the market. ULIPs come with a combination of tax benefits and life coverage. Under section 80C of the Income Tax Act, you’ll be entitled to receive tax rebates on all paid up premiums. Likewise, all of the payouts that you receive are entitled to tax exemption under section 10D. Besides seeing your money grow, you’ll be happy with how much you’ll save in the end.

Tags:

banks,

Debts,

Financial Assistance,

Funds,

Income Tax,

insurance,

investments,

money,

personal finance,

Premiums,

Stocks

April 13, 2017

If you buy a prebuilt home that doesn’t have a tremendous value as it stands, you might find yourself wondering whether to rebuild it from the ground up or try to repair and remodel it as it stands. The question is one worth considering seriously because there can be major variations in the cost difference between the two options. There are many factors involved in the final decision according to sites like thepattisallgroup.com, each of which can influence it in a certain way.

If you buy a prebuilt home that doesn’t have a tremendous value as it stands, you might find yourself wondering whether to rebuild it from the ground up or try to repair and remodel it as it stands. The question is one worth considering seriously because there can be major variations in the cost difference between the two options. There are many factors involved in the final decision according to sites like thepattisallgroup.com, each of which can influence it in a certain way.

Historical Value Must be Checked

People commonly want to demolish and rebuild if the home they bought is a timeworn one. In cases like this, you have to think about the significance of the house in history. Some homes are protected by the city for their historical value. These are commonly referred to as heritage homes, and you can’t just take a wrecking ball to them. You must talk to the state and federal government and get permits to break them down before doing so. In times like this, it might be more convenient just to renovate the home instead.

Consider Local Building Limitations

Some parts of a town, state or country have certain restrictions placed on how you can rebuild the home after demolishing it. These are usually regions of architectural importance, which are visited by tourists often for a look at the homes which are of a certain basic design. Demolishing an old home might not be the best idea if you are required to rebuild it in almost the exact same way that it looked before.

Saving Money on Renovation Isn’t Easy

Most legitimate home improvements are quite costly. You may be tempted to save money by cutting corners on certain aspects of the renovation. However, if you ever try to sell the house in the future and the quality of even the tiniest aspect isn’t up to par, you will have to pay a pretty hefty fine to repair the house before selling it. Because of this, your long-term costs can still be far higher than when demolishing and rebuilding the house.

You Can’t Live in the House While Renovating

Many people choose renovation because they want to move in as quickly as possible. They think that staying in the home while it is being renovated is a good idea and one that will save on rent money. The truth is, this can be quite harmful to the health of the people in your home. Renovation releases toxic chemicals, dust, and worse. All of these can be harmful, especially to pets, kids, and people with allergic conditions.

You should also consider how good you are at planning things. There are people who are great planners and others who are terrible at it. If you’re a terrible planner, renovation might not be the best idea since you won’t be able to determine how well the project goes. Hiring an architect and demolishing the old house might be the best course of action in a situation like this.

Tags:

budgeting,

Business,

Costing,

expenses,

Funds,

Home,

money,

savings

January 15, 2017

Try, for a moment, to think of a corporation that compares to Apple. What company has the name recognition, branding, and carefully constructed image that Apple has built over the last decade of total technological dominance?

Try, for a moment, to think of a corporation that compares to Apple. What company has the name recognition, branding, and carefully constructed image that Apple has built over the last decade of total technological dominance?

The Leader of the Pack

The answer, of course, is that Apple has no real competition. Their rise to power has been slow and steady, but the cell phone industry analysis is indisputable. As of mid-2015, CNet reports that about 100 million Americans use iPhones. That’s roughly 1/3 of the population of the United States.

If you walk into your local coffee shop, you’ll immediately note the dominance of the MacBook as the preferred notebook computer for telecommuters across the US. Want a tablet? The iPad is the obvious choice.

The popularity of a product is one of the most important variables in determining whether there is money to be made in servicing and repairing that product. Consider other household goods, appliances, or even vehicles? If a car manufacturer produces a dominant model, and that model is purchased and driven by 1/3 of the US population, how many other services professionals can benefit from that popularity? Mechanics will exclusively service the model. Aftermarket part manufacturers will build and distribute exclusively for the model and re-sellers will benefit from exclusively carrying the model, since such a huge percentage of the population will purchase it.

Using the auto analogy helps to demonstrate the significant opportunity that exists for an iPhone repair franchise. Sure, cars cost more. But the impact of Apple’s popularity is difficult to comprehend without thinking in terms of other, similarly valuable products.

Apple Franchise Markets are Everywhere

One of the secrets to successful franchising is selecting an appropriate market in which to operate a new business. For some franchises, that decision can be tricky. Food preferences can depend on region. Educational and fitness needs are largely dependent on demographics like age and income. But Apple products, with their complete market domination, are present in every metro area and suburb, every college campus and retirement community. Uses vary, certainly. The average MacBook pro user will differ significantly from the average owner of an iPhone manufactured three years ago. Their repair needs, however, are universal.

Refreshed Apple Products as an Income Stream

Making money with an iPhone repair franchise is possible in part because of the multiple income streams that are generated by a familiarity with the products and the capacity to fix them. One of those income streams is the sale of refreshed products, which come in as trades for customers in search of an upgrade. Although we’re accustomed to hearing about how high-tech goods are out of date as soon as they are purchased, there are several reasons that consumers have proven to be quite interested in purchasing used or refurbished Apple electronics.

- Upgrades are largely software based. From one generation to the next, cell phones, tablets, and computers no longer change physically by leaps and bounds so that they quickly become obsolete. Instead, Apple (along with its competitors), rolls out downloadable software updates that keep even older hardware running for many years.

- New products are prohibitively expensive. Thousands of dollars for laptops. Hundreds of dollars for even the cheapest cell phone in the lineup. Apple products are extremely expensive, but that has done nothing but whet the public’s appetite for them. Middle-income consumers have kept the prices of used and refurbished Apple products steadily high for years, with online and iPhone repair franchise profits significantly greater, as a percentage of original retail pricing, than any other comparable goods. A car driven off the lot loses a third of its value immediately. A brand new iPhone does no such thing.

- Many repairs are easy. Broken screens and dead home buttons are often enough to send consumers—accustomed to instant gratification from their expensive devices—running to order a new tablet or phone. But the repairs are often simple and largely cosmetic, which means excellent profit margins on refreshed items. Frustrations with non-working features or broken exteriors often mean upgrades for buyers, but for an iPhone repair franchise they mean quick turnover, minimal investment, and exceptional profits.

Selling refreshed Apple products is worth investigating for any savvy entrepreneur as a personal experiment—list an item online for sale—something in a desk drawer that you’ll never use again—and look how quickly buyers flock to purchase your used electronics. It’s a lesson that warrants reflection.

Tags:

Business,

Capital,

Earnings,

economy,

Funds,

money,

Profits,

stock

July 21, 2016

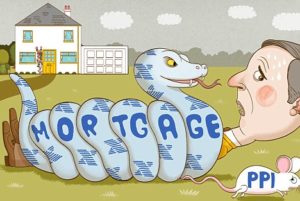

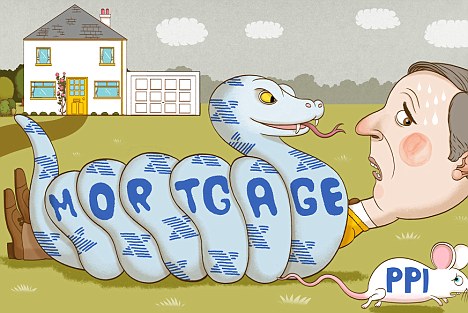

When taking out a personal loan, opening up a credit card or even taking up a mortgage, many often sign a PPI. However reality is that many are usually unaware of this fact, until they are unable to make the needed payments as scheduled. But what is a PP1?

When taking out a personal loan, opening up a credit card or even taking up a mortgage, many often sign a PPI. However reality is that many are usually unaware of this fact, until they are unable to make the needed payments as scheduled. But what is a PP1?

What Is PPI?

Short for payment protection insurance, PPI is normally sold by financial institutions to their customers as a means to protect them in the event they are unable to pay their loans. This is whether the reason behind it is sickness or loss of job. The insurance sometimes goes by the name unemployment coverage, sickness coverage or accident coverage but can broadly be referred to as credit protection insurance.

How to Get PPI money back?

In the event you have coverage and intend on getting your money back as the need has arisen, getting your claim submitted is the first step. This way information regarding just how much PPI has been sold to you on your loan and the amount payable will be revealed. In the end after the necessary paperwork has been completed, you will receive your PPI refund money back.

How much can one claim?

The amount of PPI you can claim largely depends on the amount of loan and credit card balance you have. This simply means the larger the loan and credit card balance, the bigger the PPI refund. However to know the exact amount you will need to make and offer and add the interest to know just how much you are entitled to. Take into account where you have gotten your mortgage from, all places you have taken loans from and credit cards that you have signed up for over the years. This way if you have ever signed up for PPI, the retrieval process will begin.

How far back can you claim?

In this case also there is usually no set limit. With some, register claims can be made as far back as 12 years with many having a maximum of 15 years. However you will only know whether you can get your funds back by making a claim as far back as you can. This way ensure you gather all your paperwork on the accounts you bought PPI.

How Soon Can You get your money back?

There is usually no set limit on how long it will take to return the funds to customers. However on average the time usually takes about 8 weeks. This still depends on the bank, its procedures and your history with the bank.

Filing a claim

The process of making a claim to get a PPI refund is no doubt long and tiring. In this case to make the process easy using iSmart is ideal. With the services being particularly free, you will not be charged to check whether you have a PPI on your loans. In addition no charges will be brought to you in case you chose another company to file a claim, even after knowing how much you can get as refund. Still with some lenders taking as many as 2 months to respond whether your claim can be made or not, leaving it to the professionals is better saving you time and money. As if that is not enough with PPI scandals affecting many people in the past decade, ppirefund.co.uk will ensure that even after your complaint has been rejected, you get the needed advice on what to do next.

Tags:

Business,

Credit Card,

Funds,

insurance,

investments,

money,

mortgage,

Payments

Understanding the viability of bluechip funds can help you plan your investment and get a well-rounded portfolio.

Understanding the viability of bluechip funds can help you plan your investment and get a well-rounded portfolio.

Recent Comments