January 23, 2014

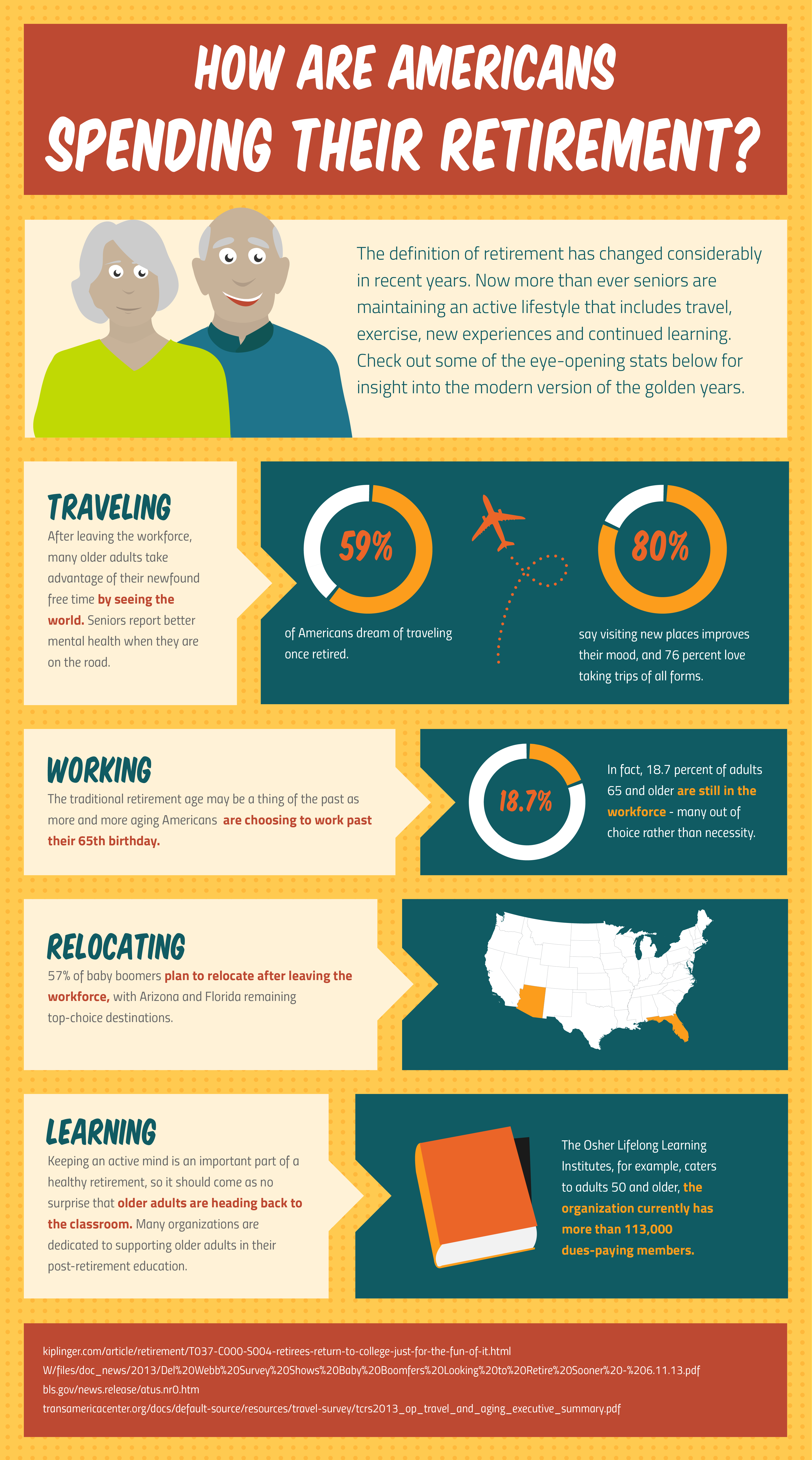

The commonly held perception of retirement living is rapidly changing. No longer are older adults settling down after leaving the workforce. Today’s retirees are more focused on active living, whether in the form of exercise, volunteering or picking up a new skill. These new trends will certainly have an impact on the financial strategies of the nearly 10,000 baby boomers turning 65 each day. Here’s a look at how the latest generation of retirees plan on spending their golden years.

Tags:

budgeting,

Interest Rates,

money,

Retirement,

Retirement Savings,

savings

November 15, 2013

Are you stuck under a pile of credit card bills, student loans or a mortgage? You are not the only one. Across the world, people are struggling to come to terms with and control their debt. The worst part is when all your debt accounts are handed over to a collections agency and they come calling at your door. With all their harassment and insults, they make you feel like it’s the end of the world. Don’t worry and remember that it’s all a part of the game they play to get their job done.

Are you stuck under a pile of credit card bills, student loans or a mortgage? You are not the only one. Across the world, people are struggling to come to terms with and control their debt. The worst part is when all your debt accounts are handed over to a collections agency and they come calling at your door. With all their harassment and insults, they make you feel like it’s the end of the world. Don’t worry and remember that it’s all a part of the game they play to get their job done.

Before all this starts happening, the best thing to do is take a reality check. The moment you realise that your debt situation is out of control, start thinking of ways to control it. There are ways and means on how to negotiate debt settlement.

Deal with the collectors

Face up to these guys and come to a settlement. What are some of the considerations while dealing with the collectors?

- Get the priorities right. When you decide on giving money to your creditors, first make sure that all your basic needs are covered. After keeping aside money for food, lodging, medicines, etc, then you start prioritizing the debt that you need to pay off. Never get intimidated by the collectors.

- Keep records. When it comes to money matters, make sure you have records of every deal and interaction along the way. All the letters, the e-mails, must be saved. Try and avoid voice interactions as much as possible and keep the correspondence written. Whenever any agreement is made, make sure it’s all in black and white and signed by the appropriate authorities.

- Again, don’t be coerced into paying more than what you can realistically afford. Don’t be taken in by the demands of the collectors and always offer to pay less than what you can actually afford. Always appear to be in control of the situation. If you show your vulnerability, they will zone in and try to take advantage of your weakness. This is one of the prime rules in how to negotiate a debt settlement.

Getting the services of a debt settlement company

Do you feel that confronting credit sharks is not in your style? Then you can always hire a company to deal with your creditors and do the negotiations. Again, step very carefully when you are hiring a company. Only hire a company with a good, solid reputation. Always go by referrals and recommendations. Remember that a respectable company wont need to solicit services through telemarketing and email blasts. They will rely on their good reputation through a steady clientele.

One important question to ask yourself before hiring a firm is whether their fees will add to your existing debt or actually sort out your debt problems? Be sure to get a clear picture of what their fees are and how those are being charged. Get it in writing to avoid grey areas.

Be well informed and aware

Make sure you are protected by knowing your rights. The more informed you are, the stronger your position will be. No one will be able to take you for a ride. You can get free data on debt settlement firms and collectors, from bodies like the state attorney general’s office, the FTC and so on. Then you will know what these people are allowed to do and not, with your debts. Get information about the debt settlement firms from your local Better Business Bureau before taking any definitive steps.

Act on time, and your future will be a steady one.

Ashton is a reputed freelance writer on topics like finance, debt and real estate. He has been published in internationally known publications over the past five years, where he has written articles on how to negotiate debt settlement. Ashton loves watching fantasy movies.

Tags:

budgeting,

Debt Negotiation,

Debts,

economy,

financial planning,

money

October 21, 2013

Anyone who is serious about their money needs a professional financial consultant to advise them on their personal finance. Many people simply need a little extra help, as not everyone is an expert on financial issues. Financial advisors give advice concerning investment strategies, mutual funds, bonds, and stocks. A good financial consultant is invested in your best interests, and wants to help you move on from your debt and budging issues. Meredon Consulting have created a list of five skills a good financial consultant must have, in order to look out for their clients best interests for the future and maximise their savings.

Anyone who is serious about their money needs a professional financial consultant to advise them on their personal finance. Many people simply need a little extra help, as not everyone is an expert on financial issues. Financial advisors give advice concerning investment strategies, mutual funds, bonds, and stocks. A good financial consultant is invested in your best interests, and wants to help you move on from your debt and budging issues. Meredon Consulting have created a list of five skills a good financial consultant must have, in order to look out for their clients best interests for the future and maximise their savings.

Education And Certification

A good financial consultant needs a bachelor’s degree in accounting, finance, or business. Knowledge of information such as estate planning, insurance investments, retirement planning, and risk management are extremely important. You don’t necessary need a certificate from the Financial Planner Board of Standards, as there is little government regulation of the industry, however certification can give your clients peace of mind and assure them you operate by a standard code of ethics. A master’s degree is useful of you want to work for a financial; firm rather than setting up your own personal business.

Extensive Knowledge

It is an extraordinary fact that many financial consultants don’t actually know a whole lot more than anyone else when it comes to the stock market. They might know why prices fluxuate, and have many theories, but they aren’t 100% sure. A good financial consultant will tell you of their uncertainties while giving you confidence and putting you in the best possible position to succeed.

Attentiveness

No matter what industry you’re in, and especially when money is involved, customer service is extremely important. Your clients will be expecting your complete attention, so you need to return their phone calls and remain attentive at all times. Meet with your clients as regularly as you can to establish rapport.

Relationship-Management Skills

It’s important to have successful people skills and be able to understand different personality types, how to resolve conflicts, how to educate people, and how to counsel clients. Clients need an unbiased financial consultant who understands their personal needs and knows how to help them make financial decisions.

Skills, Interests And Qualities

To become a financial adviser, you will need to have significant skills, interests, and qualities that relate to your clients. These include an interest in financial products and markets, the ability to explain complex information clearly and simply, excellent communication and listening skills, accuracy and attention to detail, the ability to analyse and research information, good sales negotiation and report writing skills, determination and motivation to meet targets, good mathematical and computer skills, and discretion and a trustworthy manner.

Financial planning is a challenging career that requires a wide range of knowledge, skills, and abilities. These five skills are important for a good financial consultant to know and understand in order to operate in a professional and successful manner.

Tags:

economy,

Financial Advisior,

financial planning,

money,

personal finance

October 5, 2013

Considering our invest goals is our very first step towards a successful investment. In order to choose your best investment option, you must determine the investment type that suits your requirements. Both investing and saving need to be defined ahead of all other things; in comparison to a long term engagement like investing, saving is an engagement for a short period.

Considering our invest goals is our very first step towards a successful investment. In order to choose your best investment option, you must determine the investment type that suits your requirements. Both investing and saving need to be defined ahead of all other things; in comparison to a long term engagement like investing, saving is an engagement for a short period.

Expenses like going out on vacations, paying fees for college tuitions, making a down payment for your home and buying a car are included within your saving goals. When it comes to savings, certain conventional investments may seem inappropriate as their value tend to fall with time. For successful asset management, you may seek guidance from an experienced financial adviser. CDs or online savings accounts that yield high returns may be considered as good options to secure your long time savings. You must compare various interest rates offered by online banks.

A proper financial planning takes all long term goals into accounts e.g. college tuition, inflation, retirement and other common investment objectives. Investing and saving are two categories that college tuition listed under them. The time frame you’ve selected will determine the group under which you’ll place each of them. Investments worth an intermediate length may demand more risks. For instance, you may take more risk towards investing money saved on your daughter’s college fund when he’s 10 years old than when she turns 18.

Pick the right investment vehicle

Your asset management plans turn successful once you pick the right investment vehicle after considering all major goals of investment. Remember, it’s not about jumping to the most lucrative offer that comes your way. You may begin with options that seem more interesting and funny like brokerage accounts, college saving funds, 401k plans and IRAs. Investment plans are usable only when they possess certain incentives or tax breaks for your benefit. Through your retirement years, you may enjoy tax breaks only when you choose retirement plans with tax advantages initially e.g. 401k and IRAs. For college savings you may opt for Coverdell ESAs and 529 College Savings Plans.

Open your investment account

An investment accounts needs to be opened as soon as you pick your investment vehicle and analyze your investment goals. It will just take a few minutes for you to start an IRA or get enrolled your 401k; it’s almost that simple. Opening your brokerage account could just be another option for you. It’s really simple to open your investment account; all you need to do is to fill out your information, sign it and shift funds to the account. Picking the best investment option often depends on identifying your investment types correctly!

Tags:

budgeting,

financial planning,

Funds,

investments,

money,

Returns,

savings

September 1, 2013

In the UK the Archbishop of the Church of England has struck out at pay day lenders calling them “morally wrong”. Unfortunately after bashing the pay day loan industry it transpired that the Church had invested over $7 billion of its pension funds in a company which had then supported a pay day lender. Indirectly therefore the Church had invested in a pay day lender! The very industry it regarded as sinful. It seems they were suitably embarrassed.

In the UK the Archbishop of the Church of England has struck out at pay day lenders calling them “morally wrong”. Unfortunately after bashing the pay day loan industry it transpired that the Church had invested over $7 billion of its pension funds in a company which had then supported a pay day lender. Indirectly therefore the Church had invested in a pay day lender! The very industry it regarded as sinful. It seems they were suitably embarrassed.

In response to the Archbishop’s attack the pay day lender in question, Wonga, who is also a pay day loan provider in Canada (see www.Wonga.ca), created and released a very clever, tongue in cheek, advertisement based on the 10 commandments – the Wonga version is the 10 commitments. The aim of the advert is to better educate people when interpreting the Church’s comments about pay day lenders. It sets out the promises the company makes to its borrowers and highlights the fact Wonga is a responsible lender. Probably the Church is a little unhappy that the debate and the new advertising campaign has certainly given the lender even more publicity – the adverts have of course been reported upon by the media thus resulting in free advertising and increased publicity for the company.

Further, far from sounding like the loan shark the Church has tried to portray pay day lenders as, the Wonga advert pretty much agrees with what the Church has had to say on the issue of pay day lending. The lender stated it was transparent about the price of its loans, carried out thorough credit checks and froze interest after two months to protect defaulting customers. It also said that it welcomed competition.

The pay day loan industry in the UK is not regulated like it is in Canada. Many politicians, charities and other organisations are calling for regulation but do not have the solution – the Archbishop is at least trying to push forward an idea. He is proposing that Credit Unions work from church premises to offer similar loans at lower interest rates – his idea is to push pay day lenders out of the market. This certainly sounds like a challenge. For a start he wants to find church members to volunteer as staff at the branches. This may be a big hurdle in terms of attracting customers. The average church goer probably does not reflect the average pay day loan customer. No one wants to be judged when taking out a loan.

A recent study indicated that the average age of a church goer was 61. Anglican leaders have warned that the Church of England will cease to exist in 20 years because elderly worshippers will die. As a result of this the Church presently has an urgent national recruitment drive to attract more members.

Just recently the Rt Rev Paul Butler, Bishop of Southwell and Nottingham stated that teachers should not illustrate math lessons with examples of “profit and loss”, or encourage children to save in order to buy bikes or toys Instead, lessons should focus on the math involved in giving donations to charity, saving for an overseas project, or even “tithing” – giving 10 per cent of one’s income to the Church.

When the Church is making statements like this you have to wonder whether it is the Credit Union/pay day loan “solution” is one part of its necessary recruitment drive. Pay day loan providers want profit, the Church wants people in seats: both have their own agenda.

Although the Rt Rev Paul Butler might not think it important, educating children about profit and loss and savings is all part of money management. This is vital in today’s society – Surely it is better money management which will reduce the need and desire for pay day loans.

Tags:

Cash Flow,

Debts,

financial planning,

Interest Rates,

loans,

money,

payday loan

Recent Comments