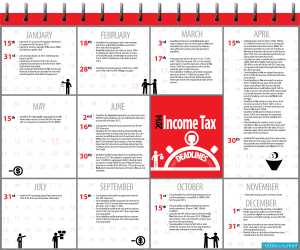

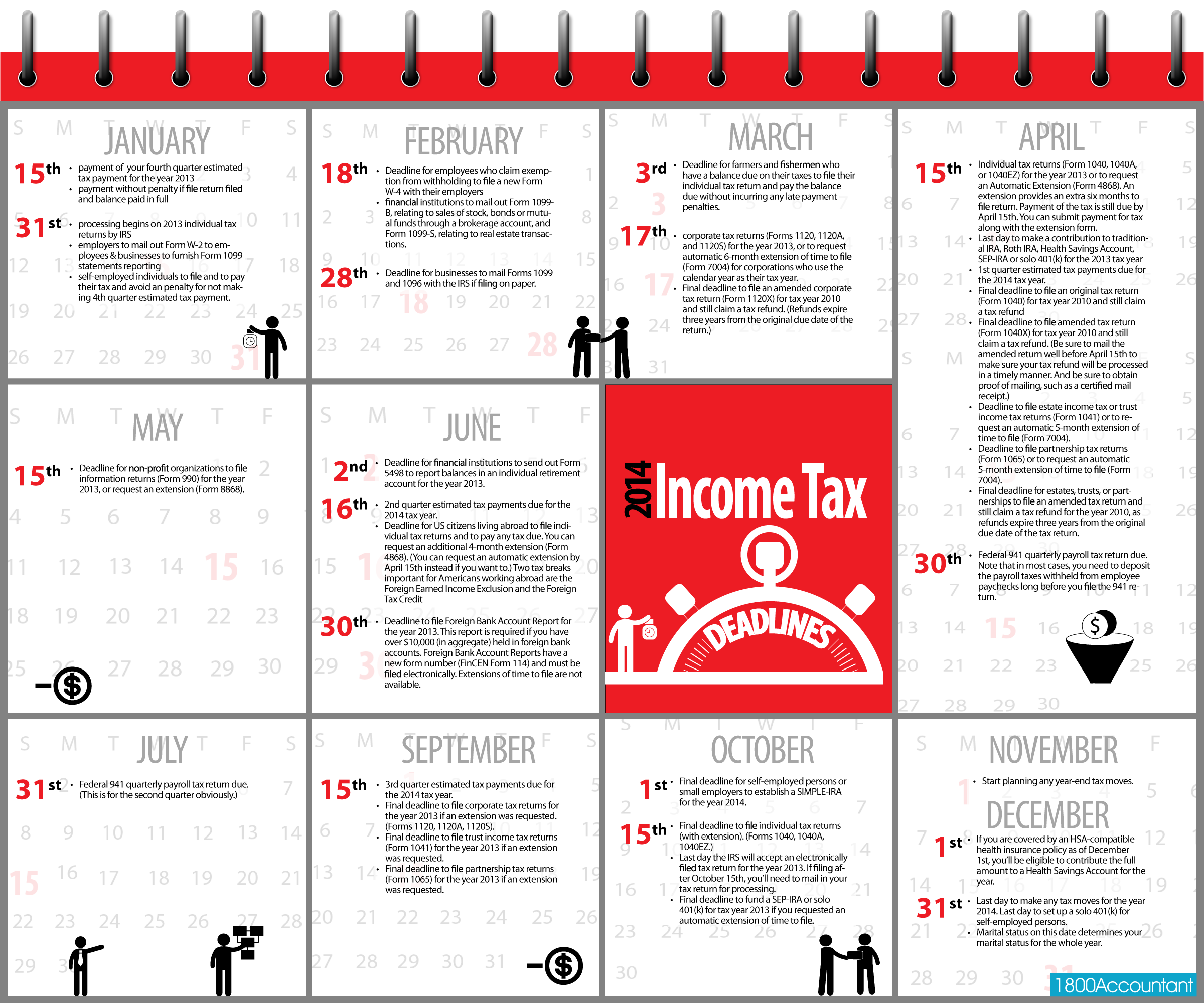

February 7, 2014

Hands up if you’ve got your tax act together! What? No hands up? Well then, grab a seat and listen up!

The State and Federal governments have set up certain due dates for filing or e-filing your taxes. To some, understanding taxes and meeting tax deadlines is the first among many horrifying aspects of filing tax returns. But once you understand when and what needs to be filed, it will be the first big step you’ve taken towards de-horrifying the process of tax filing and returns.

April 15th is a big date to remember. Not only must you file your taxes by this day but you also need to pay an estimate of any taxes due. 11.59 pm on that day is the deadline. Miss that and you’ll need to request an extension from the IRS. And even if you do request an extension, remember you still need to pay the taxes you owe.

In addition to that big date, there are several due dates to keep in mind depending on your status – whether you’re individual tax payer, a business (S corporation, C Corporation or LLC) or a charity. The infographic below will help you keep a track of those dates. Remember, if a filing date falls on a weekend or a national holiday, the date will be moved forward to the next working day. It’s important not to miss these dates because if there’s one thing you don’t want, is the IRS on your back, right?

What happens if you don’t meet the deadline?

Brace yourself! This is the next horrifying part of filing taxes. A lot. A lot of bad things can happen if you don’t meet that deadline. For one thing, the fee for not filing is a lot harsher than it is for late filing. In addition, there are penalties which you can check out on the IRS website.

What Not to Forget

You’d be surprised at the common mistakes people make when filing their taxes. Before you send those papers to the IRS double check whether you’ve:

• Put a stamp on the envelope

• Signed the documents (Don’t laugh. It happens more often than you’d think)

• Included the social security numbers of their children and adult dependents

• Annual limits and tax tables can change from year to year. Make sure you’re using the right.

If you run a small business, there’s a never-ending string of dates that you have to keep in mind. Make entries in your PDAs, your laptop and any other devices you use to keep your appointments to help you stay on top of things.

What to Remember

Remember to take advantage of tax deductions. These may change from year to year as well and I sometimes suspect it is in the IRS’s best interests to confuse us folks! It may help to hire professional accounting firms whose job it is to prepare and file your returns while maximizing your earnings. Firms, like 1800accountant, designate a personal accountant to your case and offer 24/7 access the whole year round. It’s worth looking into such services and enjoy the peace of mind that comes from knowing you’ve got your taxes taken care of and managed to make some tax savings. Now that’s what I’m talking about. 🙂

Tags:

budgeting,

economy,

Income Tax,

money,

tax

January 9, 2014

A sustained bull market has equity investors anticipating a lucrative 2014. A weak dollar and low interest rates are among several factors that bode well for corporate profits in the New Year.

A sustained bull market has equity investors anticipating a lucrative 2014. A weak dollar and low interest rates are among several factors that bode well for corporate profits in the New Year.

With a low dollar, export driven companies can expand into overseas markets by competitively pricing their products. To raise money, companies can issue low coupon bonds that easily exceed the yields of low risk treasuries. Robust venture capital has non-traditional borrowers turning to Elliott Broidy and other financiers for needed capital.

The past several years have seen many investors chase returns and buy securities with the strongest short term performance. As a result, many investor portfolios have grown to reflect the broader market.

Fortunately, there are convenient ways to reduce the risk of a portfolio that moves in lockstep with equity markets. Beyond hedging, these investments may be suitable as mainstays in your portfolio.

Below are some strategies to consider:

Intermediate Bonds:

Low yields are posing challenges for income investors. Risk free treasuries offer safety but little income. The rock bottom treasury yields make it affordable for non-government bonds to compensate investors for added risk. Investors should also have perspective on the impact of interest rates rising in the future.

Bond maturities of 3 to 10 years offer an attractive hedge for several reasons. These bonds add negative correlation by mostly moving in different directions from the broader market. Intermediate maturities are also attractive when there is uncertainty about interest rates.

It is unlikely that short term rates determined by the Federal Reserve will head any lower. Similarly, when and if rates will rise is also uncertain. Intermediate bonds allow you to earn yield above that of shorter maturities, without the interest rate risk of long term debt, which would be battered by rate hikes.

For most investors, mutual funds are a convenient way to buy intermediate bonds. You should review the credit quality and interest rate sensitivity of bond mutual funds through Morningstar or Bloomberg.

Depending on your risk tolerance and income needs, international bond funds may also be an option. If you plan to draw income, interest payments from stronger currencies will be increased when converting into dollars.

Real Estate Investment Trusts (REITs):

Do you want real estate exposure without the hassles and expense of owning investment property? You should consider exchange traded REITs as an affordable and liquid alternative.

These publicly traded securities are required by the IRS to pay out 90% of taxable income to shareholders. Income starved investors appreciate that many REITs currently feature yields over 6%, with some international options paying double digit yields.

Real estate is a volatile asset class that often moves separately from equity markets. However, the cash, financing and time needed is beyond smaller investors. Unlike owning real estate, REIT shares can be easily bought and sold. You can quickly take and unwind positions as investment goals or real estate markets change.

REITs also allow you to capitalize on demographic trends such as an aging population or healthcare laws. Investing in REITs that specialize in elderly care facilities or geographic regions with thriving real estate markets are examples of this.

To soften volatility, you may choose hybrid REITs that collect rent payments and also earn mortgage interest. With lending and rental revenue, a hybrid REIT is more poised to benefit from different real estate trends.

Low cost and the ability to diversify make ETFs or mutual funds suitable for most REIT investors. International REITs give you access to overseas property markets. Similar to overseas fixed income, dividend payments from foreign REITs may be increased in dollar terms. Your currency adjusted returns could also be higher during times of dollar weakness.

Summary:

Portfolio rebalancing can include adding small doses of volatility to reduce the overall risk in your portfolio.

By considering the impact of a bull market on sector weights, market cap and asset exposure; you gain better perspective for changing conditions.

Tags:

Business,

economy,

Foreign Exchange,

Forex,

investment

November 26, 2013

There are many reasons why it can sometimes be a good idea to borrow money. It can make it possible to invest in assets in a way that makes financial sense – for instance, taking advantage of a discount on a new sofa that’s really needed, where the saving amounts to more than the interest on the loan. It can be about consolidating debt, using one big loan to pay off several smaller ones, which often results in lower overall interest payments and better terms and conditions. In some situations, it can be necessary to meet ordinary household expenses whilst waiting for a salary payment, especially if one has a variable income or creditors that are slow to pay. Getting a loan to pay for transport costs can also make sense by making it possible to stay in work and thereby keep bringing some money in. Whatever the reason, it’s something that should be approached with caution – and with a clear plan for paying the money back firmly in place.

There are many reasons why it can sometimes be a good idea to borrow money. It can make it possible to invest in assets in a way that makes financial sense – for instance, taking advantage of a discount on a new sofa that’s really needed, where the saving amounts to more than the interest on the loan. It can be about consolidating debt, using one big loan to pay off several smaller ones, which often results in lower overall interest payments and better terms and conditions. In some situations, it can be necessary to meet ordinary household expenses whilst waiting for a salary payment, especially if one has a variable income or creditors that are slow to pay. Getting a loan to pay for transport costs can also make sense by making it possible to stay in work and thereby keep bringing some money in. Whatever the reason, it’s something that should be approached with caution – and with a clear plan for paying the money back firmly in place.

Borrowing options

The simplest way for most people to borrow money is by getting a loan from the bank, but rates can vary a lot and people with poor credit records may struggle to do this at all. Social fund and credit union loans can be a good bet but what’s available can vary by location. The Citizens’ Advice Bureau can provide guidance on this. Credit card loans can sometimes be a good way to borrow, within agreed limits, but can be very expensive if not paid back on time. Payday loans with dedicated lenders work for many people but should not be taken on without a careful assessment of what their interest rates really mean if you are late in paying. Store card loans are sometimes worthwhile when they also offer deals or discounts, but can be very expensive and should be treated with caution.

Generally speaking, loans are easier to get if secured against an asset like a house or car. These are known as secured loans. It is important to be aware that the asset could be at risk if the terms of the loan are not met. When taking out a loan it is a good idea to avoid the comfortable assumption it will be paid off on time and make a back-up plan for what can be done if that doesn’t happen.

Borrowing on a car

Thinking about the assets they have available, many people are quick to say “I’ll borrow money on my car!” As with all loans, there are good and bad ways to approach this.

Various different types of loan can be secured against a car, so it’s wise to shop around for a good interest rate. The most common type, logbook loans, mean that the lender technically owns the car whilst the loan is outstanding, but it’s still available for the borrower to drive. A good lender will not simply take the car if things go wrong but will work with the borrower to come up with a workable repayment plan.

Although they can be expensive, loans against cars generally provide a reliable way to get a large sum of money in just a few days, regardless of credit history. They’re generally cheaper than payday loans as the existence of collateral lowers the risk for the lender.

Tags:

Assets,

Car Finance,

Car Loan,

Debts,

economy,

financial planning,

Interest Rate,

loans

November 25, 2013

Many sole traders make the move to limited company status because they believe it will make them more desirable to new clients, or perhaps because they think they can save on tax in the long run. For a small limited company however, understanding how tax works is vital – and tax matters can be extremely confusing! All limited companies, both large and small, need to be up-to-date on current tax matters, as the consequences can – and often are – costly.

Many sole traders make the move to limited company status because they believe it will make them more desirable to new clients, or perhaps because they think they can save on tax in the long run. For a small limited company however, understanding how tax works is vital – and tax matters can be extremely confusing! All limited companies, both large and small, need to be up-to-date on current tax matters, as the consequences can – and often are – costly.

Limited companies don’t use the same self assessment tax return system as other businesses and self-employed individuals. All limited companies, both large and small, are subject to annual corporation tax.

This means the company does its own corporation tax self assessment – i.e. it calculates the amount of tax it must pay itself using a company tax return. The methods and deadlines are different to those used elsewhere.

The most common tax issues faced by a small limited company

It’s important to remember that once a company has applied for and been given limited company status, it is now a separate legal entity from its owner, irrespective of how many staff it employs or who is a shareholder. Everyone, even the sole director/shareholder, is an employee and the company the employer. What this means in terms of tax is that all the money the company earns belongs to the company and not its owner: from now on, any money taken out of earnings must be noted (and justified) as salary or expenses, and comes under scrutiny from HMRC.

Many small limited companies end up having to pay excess tax because the owner simply takes money out of the company without understanding the tax implications. The company can pay its director in three ways: as salary, to pay back money borrowed or spent on company costs (expenses), or as dividends on the shares the director holds in the company. Getting the mixture of salary and dividends right can reduce a company’s tax bill; get it wrong and it can go the other way.

All limited companies must pay corporation tax by the 1st of January of the year after the trading year, i.e. on 1/1/2014 for trading between 1 April 2012 and 31 March 2013. It must also file a corporation tax return (CT600) each year to HMRC, 12 months after the year end at the latest. Limited companies who fail to file their CT600s or send it too late are subject to hefty fines.

A small piece of legislation known as IR35 has also caused many small limited companies problems since coming into effect. This is when a company takes on a project for a client and takes on the status (however short-term) of an employee. Rather than pay the ’employer’s’ National Insurance on the full cost of what they paid out, the small limited company makes a ‘deemed payment’ to HMRC. This is the opposite of how it works for sole traders.

Where to get advice

Calculating taxes as a limited company is complex and can be both challenging and time-consuming. There are companies that specialise in tax management that small limited companies can turn to for advice in this field, whether a company needs help filling out its corporation tax return or with IR35 forms for employees. An umbrella company can help a small limited company with all aspects of tax and payroll and as qualified experts in all tax matters, can save time and money in the long run.

Tags:

Currency,

economy,

Employee. Financial Advisor,

financial planning,

investments,

money,

Salaries,

savings,

tax

November 24, 2013

In order to concentrate on their key areas of expertise as well as to save costs and resources in secondary areas, large companies often outsource certain tasks. The kind of tasks typically outsourced include payroll, HR services, translation/localisation of marketing materials or documents, tax administration and general administrative tasks.

In order to concentrate on their key areas of expertise as well as to save costs and resources in secondary areas, large companies often outsource certain tasks. The kind of tasks typically outsourced include payroll, HR services, translation/localisation of marketing materials or documents, tax administration and general administrative tasks.

What are the advantages of outsourcing for large companies?

The most obvious benefit of outsourcing is in cost reduction, but this should not be the only reason for outsourcing: no entrepreneur can do everything themselves, and contracting certain tasks out-of-house means one less thing for a busy company to juggle. It is also a way of getting expert assistance in a specific area without having to train existing staff or recruit new ones.

Outsourcing streamlines a business into the areas it wishes to concentrate on without having to spread resources too thinly, and a third-party supplier of HR, for example, will generally be more efficient in providing HR than a large company with many different departments. Well-trained, expert members of staff employed by the outsourcing company have access to superior technical equipment and systems and are up-to-date on current legal requirements. Outsourcing can reduce legal as well as financial risks.

When and what to outsource?

Almost everything can be outsourced, but it may not be prudent to do so. A large company should not outsource any activity that is central to generating profits or competitive success, for example; these would generally be tasks connected to the company’s brand name or core areas. For example, a company that invented a great engineering gadget should not outsource its production, but if sudden expansion put a strain on its resources, outsourcing payroll could be a sensible option.

Most large companies outsource routine tasks that waste valuable time that could be spent elsewhere, and/or temporary activities that are one-offs or occur once or twice a year and require extra resources unavailable in-house.

How are outsourcers paid?

When a large company finds a third party supplier to outsource certain aspects of their operations to, the two parties will sign a contract or Service Level Agreement (SLA) as regards payment. Outsourcers are normally paid a fixed cost for all services as defined in the contract; any additional services that may occur are charged extra.

Where are tasks outsourced?

Many tasks, including payroll solutions, IT and tax administration, can today be outsourced to a third party supplier based anywhere in the UK thanks to modern computer and communications technology that enables efficient business without the need for face-to-face contact.

How does a company find a good outsourcer?

Make no mistake: the selection process is of utmost importance. Choosing the right outsourcing partners is not only about finding the cheapest provider: the right partner must be good at what they do and be a trustworthy and legitimate enterprise. It’s also important to ensure that contracts and SLAs are written in a way that meets everyone’s needs, and that can be adjusted by the company to suit unforeseen changes should they arise.

The internet has made finding good outsourcers easier; for instance, typing get ‘tax help here’ into a search engine can bring up many qualified and reputable companies suited to one’s needs.

Tags:

Business,

Capital,

economy,

investments,

Leads,

money

Recent Comments