August 27, 2016

Graduating from a prestigious educational institution with specialized certification in accountancy? You are all set to bag your first job in your field of interest—accounting.

Graduating from a prestigious educational institution with specialized certification in accountancy? You are all set to bag your first job in your field of interest—accounting.

Applying for that dream job might be a tedious process and waiting for a call back after an interview might take several months.

Here are three of the most important things you need to take care of so you can bag a job before your potential rivals.

1. Resume

The first—and sometimes only—thing that a HR manager looks at to decide if you are worth hiring is your resume and remember you have only 6 seconds to catch their attention. As a fresher with no experience, you might not have much on there. This means you need to figure out what content goes in your resume.

Choose an apt font and size that gives it a classic and clean-cut professional look. With some research, you can find good resume keywords online, including those that help catch the attention of the hiring committee. Avoid using capitalized, bold, and italicised terms in you bio, unless absolutely necessary.

Pick the perfect type of resume that allows you to highlight your skills and specializations. Chronological, functional, and combinational are three of the basic types of resumes among a list of many others.

Use catchy subtitles. Construct lines effectively. Do not write more than two lines for any description, and keep the language stylish yet simple. Watch carefully for grammatical errors.

Make sure you don’t go overboard with any of these tips. Your resume should portray effortless efficiency. Also, try to keep it within 2 pages.

2. Interview

Once your resume is selected, you’ll have to face the interview. Most people get nervous and anxious, and tend to mess up their interview despite their calibre and talent. This is mainly due to lack of preparation. Even though most interviewers expect you to be street-smart, a thorough knowledge in the field of your choice is also essential.

You are spoiled for choices when it comes to resources—be it online or offline—to help your prep for the interview. You can easily find blogs that give out frequently asked interview questions in a finance interview.

Apart from preparing for these questions and brushing up on your syllabi that was covered over the many semesters, you should also have a brief knowledge of software like ERP accounting software and business management software that are in trend, and are used by most organizations.

Knowledge about current affairs and the latest accounting standards is also an absolute necessity.

3. Confidence

To crack any interview, confidence is the most important factor. Your body language plays a significant role in cracking an interview. Even small signs of nervousness or uncertainty are caught during the interview. Stay confident right from when you send out your resume. The process might be a time-consuming one, but leads to success.

With some motivation, patience, and making smart choices while displaying your talents, landing your dream job is a piece of cake. Use these tips, and an accounting job is in the bag!

Tags:

Accounts,

Business,

Capital,

economy,

investments,

money

August 10, 2016

Many homeowners have a considerable amount of cash tied up in the equity of their homes – that is, the value of the amount of the home they own, less any outstanding mortgage or loan.

Many homeowners have a considerable amount of cash tied up in the equity of their homes – that is, the value of the amount of the home they own, less any outstanding mortgage or loan.

Not only is it possible to release that equity – to enjoy its present cash value – but more homeowners than ever before appear to be choosing to do so. This is a conclusion drawn in a story published in the Guardian newspaper on the 25th of January 2016.

During the course of 2015, a record 22,500 equity release agreements were made, representing a return to the nation’s homeowners of a total of some £1.61 billion.

How do I know if equity release is right for me?

Probably the single most informative source is an online equity release calculator. It might be the best step to gaining some idea of what equity there may be in your home that may be released, depending on the value of the property and your age (you need to be 55 or over to qualify for any equity release scheme).

Combine an equity release calculator with a comparison website which shows the various interest rates currently offered by equity release providers and you may get a pretty clear idea of whether to take things further. There is generally no limit on the number of times you may use the same calculator.

There are any number of such online calculators and it might be difficult knowing which one to choose. Some of the things to look out for when choosing one, therefore, might include:

- how much equity you might be able to release, the interest rates governing the various schemes on offer and what the impact is likely to be upon your estate;

- whether the provider is a member of the Equity Release Council – since this guarantees a certain number of safeguards built into any agreement; and

- whether the site providing the calculator also offers a detailed guide on how equity release works and the arrangements that might be made to answer your queries and discuss your concerns directly with any provider.

Types of equity release

Using an equity release calculator is only the first step in what is invariably a complicated process, involving very serious decisions about the home in which you live, the funds it might unlock and the impact any agreement has on the estate you may pass on to your surviving dependents and relatives.

This makes it important that you seek the advice and guidance of a specialist in the provision of equity release agreements and embark on a learning curve that might lead to your understanding of the two principal vehicles for equity release:

- home reversion – this involves the sale of a proportion of your home to the equity release provider, so that you become a co-owner, but may continue to live in the dwelling until your share of the property is sold upon your death or when you move into long-term care; or

- lifetime mortgage – this is probably a more popular arrangement than home reversion and allows you to make a more reliable calculation of the costs involved. A lifetime mortgage is similar to a regular mortgage, but you make no repayments on the advance, which continues to attract interest in the normal way. The mortgage is repaid from the sale proceeds of the property when you die or move into long-term care.

The use of an equity release calculator may be enough to set you off on the road to unlocking some of the wealth tied up in your home.

Tags:

Business,

Equity,

financial planning,

investments,

money,

stock

July 21, 2016

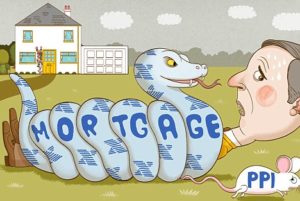

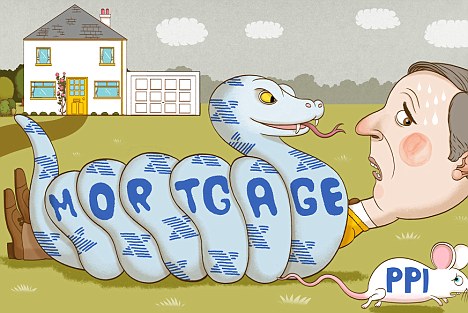

When taking out a personal loan, opening up a credit card or even taking up a mortgage, many often sign a PPI. However reality is that many are usually unaware of this fact, until they are unable to make the needed payments as scheduled. But what is a PP1?

When taking out a personal loan, opening up a credit card or even taking up a mortgage, many often sign a PPI. However reality is that many are usually unaware of this fact, until they are unable to make the needed payments as scheduled. But what is a PP1?

What Is PPI?

Short for payment protection insurance, PPI is normally sold by financial institutions to their customers as a means to protect them in the event they are unable to pay their loans. This is whether the reason behind it is sickness or loss of job. The insurance sometimes goes by the name unemployment coverage, sickness coverage or accident coverage but can broadly be referred to as credit protection insurance.

How to Get PPI money back?

In the event you have coverage and intend on getting your money back as the need has arisen, getting your claim submitted is the first step. This way information regarding just how much PPI has been sold to you on your loan and the amount payable will be revealed. In the end after the necessary paperwork has been completed, you will receive your PPI refund money back.

How much can one claim?

The amount of PPI you can claim largely depends on the amount of loan and credit card balance you have. This simply means the larger the loan and credit card balance, the bigger the PPI refund. However to know the exact amount you will need to make and offer and add the interest to know just how much you are entitled to. Take into account where you have gotten your mortgage from, all places you have taken loans from and credit cards that you have signed up for over the years. This way if you have ever signed up for PPI, the retrieval process will begin.

How far back can you claim?

In this case also there is usually no set limit. With some, register claims can be made as far back as 12 years with many having a maximum of 15 years. However you will only know whether you can get your funds back by making a claim as far back as you can. This way ensure you gather all your paperwork on the accounts you bought PPI.

How Soon Can You get your money back?

There is usually no set limit on how long it will take to return the funds to customers. However on average the time usually takes about 8 weeks. This still depends on the bank, its procedures and your history with the bank.

Filing a claim

The process of making a claim to get a PPI refund is no doubt long and tiring. In this case to make the process easy using iSmart is ideal. With the services being particularly free, you will not be charged to check whether you have a PPI on your loans. In addition no charges will be brought to you in case you chose another company to file a claim, even after knowing how much you can get as refund. Still with some lenders taking as many as 2 months to respond whether your claim can be made or not, leaving it to the professionals is better saving you time and money. As if that is not enough with PPI scandals affecting many people in the past decade, ppirefund.co.uk will ensure that even after your complaint has been rejected, you get the needed advice on what to do next.

Tags:

Business,

Credit Card,

Funds,

insurance,

investments,

money,

mortgage,

Payments

July 5, 2016

Knowing you need money is the easy part. Getting financial assistance is more of a challenge. But it’s managing your loan once you get it that takes the cake. No one needs help spending the funds that they receive but learning how to get one that fits their financial situation can take some getting used to. Though navigating the world of rates, fees, and repayment schedules can be difficult, it’s not impossible. You can easily accommodate a small cash advance into any sized budget when you take into account the following tips.

Knowing you need money is the easy part. Getting financial assistance is more of a challenge. But it’s managing your loan once you get it that takes the cake. No one needs help spending the funds that they receive but learning how to get one that fits their financial situation can take some getting used to. Though navigating the world of rates, fees, and repayment schedules can be difficult, it’s not impossible. You can easily accommodate a small cash advance into any sized budget when you take into account the following tips.

Look for flexible options

Small dollar loans are typically anywhere between $200 and $1,000, regardless of where or how you secure one. Their repayment, on the other hand, is up for negotiation. In some states, installment loans are a flexible alternative to traditional financial products. Whereas small cash advances require immediate repayment by your next payday, installment loans are paid back in increments according to a prearranged schedule. If you live in Missouri, Maryland, or Kansas, direct online lenders normally schedule these payments according to your paydays. You can check out Moneykey.com/installment-loans-online.php to learn more about how they work in detail.

Go online

A popular budgeting tip is using e-banking to create pre-authorized payments for all of your financial obligations. It’s a simple way to avoid missing a payment, as your bank account will automatically transfer the appropriate funds to your payee. The same idea works well with your installment loan. By partnering with a direct online lender, you can make all of your incremental payments online. Never once having to wait for USPS to deliver a check or for that check to clear, your electronic payment is immediate. As long as you have the sufficient funds in your account, you won’t ever have to worry about missing a payment.

Choose a state licensed lender

Not all direct online lenders are alike, and many of them offer financial products – even flexible installment loans – that could directly interfere with your ability to repay them. These lenders provide assistance that comes at a cost, and even an incremental repayment program can’t offset their inflated rates and fees. A license issued by your state will ensure a direct online lender offers reasonable rates, fees, and conditions. When a lender is licensed, it means they meet your state’s regulations regarding the lawful size of financial products.

With a little time spent online, you can find a lender you can trust and set up pre-authorized payments for your flexible installment loan. Once you do, managing your financial assistance will no longer be a challenge. It may even be as easy as spending it!

Tags:

Debts,

economy,

financial planning,

Interest Rates,

loans,

money

June 30, 2016

As you’re leaving school, finishing university and getting your first job, retirement is most likely the last thing on your mind. But taking a few steps to set yourself up in your 20s can go a long way to avoiding financial stress in later life. It’s never too early to start preparing for your future.

As you’re leaving school, finishing university and getting your first job, retirement is most likely the last thing on your mind. But taking a few steps to set yourself up in your 20s can go a long way to avoiding financial stress in later life. It’s never too early to start preparing for your future.

Set some goals

It’s much easier to get what you want, if you’re clear about what exactly it is you want. We all want to have feel fulfilled, but what does this mean to you and how are you going to achieve it. Of course these goals may change but the planning will be the same.

Consider setting yourself some short, medium and long term goals.

Short term goals might be taking a holiday or buying a car. These are the things you should be putting money towards now, on a regular basis.

Medium term goals can set you up for the next stage in life. Will you want to buy a house, raise a family? You might not want to put all your money towards these right now but they will require planning and saving.

Long term goals will most likely your retirement. You superannuation fund will go a long way to determining this, so it’s important to ensure your employer is contributing correctly.

Pay down your debt

Putting aside savings for a car is all well and good, but any debts you have may affect your ability to reach your financial goals in the short to medium, or even long term. Don’t forget to include any debt repayments as part of your budget.

Budgeting

Budgeting doesn’t mean living on baked beans while you’re friends are out eating at a nice restaurant. What it does mean is being realistic about exactly how much money you are earning and spending. Creating a budget is the best way to track your expenses and avoid living beyond your means. Try some of these great budgeting apps to help you manage the process.

Automatic savings

Once you have created your budget and know exactly how much you have available, you can start saving for your goals. Setting up an automatic payment to a separate savings account will help keep you on track and stop the temptation to dip into your funds.

Sort your Super

For any job you hold over the age of 18 and earn more than $450 a month, or any job in which you work 30 hours or more per week, your employer pays out superannuation. Unless you specify otherwise, these workplaces pay your super to an account with their chosen super fund. Which means if you have had four different jobs, you could have as many as four different superannuation accounts, and be paying four sets of fees.

Combining these funds into the one superannuation account means you only pay one set of account fees, but also means it’s easier to track how much money you have to set you up for your retirement.

Tags:

budgeting,

economy,

financial planning,

Financial Retirement,

money,

savings

Graduating from a prestigious educational institution with specialized certification in accountancy? You are all set to bag your first job in your field of interest—accounting.

Graduating from a prestigious educational institution with specialized certification in accountancy? You are all set to bag your first job in your field of interest—accounting.

Recent Comments