August 10, 2016

Many homeowners have a considerable amount of cash tied up in the equity of their homes – that is, the value of the amount of the home they own, less any outstanding mortgage or loan.

Many homeowners have a considerable amount of cash tied up in the equity of their homes – that is, the value of the amount of the home they own, less any outstanding mortgage or loan.

Not only is it possible to release that equity – to enjoy its present cash value – but more homeowners than ever before appear to be choosing to do so. This is a conclusion drawn in a story published in the Guardian newspaper on the 25th of January 2016.

During the course of 2015, a record 22,500 equity release agreements were made, representing a return to the nation’s homeowners of a total of some £1.61 billion.

How do I know if equity release is right for me?

Probably the single most informative source is an online equity release calculator. It might be the best step to gaining some idea of what equity there may be in your home that may be released, depending on the value of the property and your age (you need to be 55 or over to qualify for any equity release scheme).

Combine an equity release calculator with a comparison website which shows the various interest rates currently offered by equity release providers and you may get a pretty clear idea of whether to take things further. There is generally no limit on the number of times you may use the same calculator.

There are any number of such online calculators and it might be difficult knowing which one to choose. Some of the things to look out for when choosing one, therefore, might include:

- how much equity you might be able to release, the interest rates governing the various schemes on offer and what the impact is likely to be upon your estate;

- whether the provider is a member of the Equity Release Council – since this guarantees a certain number of safeguards built into any agreement; and

- whether the site providing the calculator also offers a detailed guide on how equity release works and the arrangements that might be made to answer your queries and discuss your concerns directly with any provider.

Types of equity release

Using an equity release calculator is only the first step in what is invariably a complicated process, involving very serious decisions about the home in which you live, the funds it might unlock and the impact any agreement has on the estate you may pass on to your surviving dependents and relatives.

This makes it important that you seek the advice and guidance of a specialist in the provision of equity release agreements and embark on a learning curve that might lead to your understanding of the two principal vehicles for equity release:

- home reversion – this involves the sale of a proportion of your home to the equity release provider, so that you become a co-owner, but may continue to live in the dwelling until your share of the property is sold upon your death or when you move into long-term care; or

- lifetime mortgage – this is probably a more popular arrangement than home reversion and allows you to make a more reliable calculation of the costs involved. A lifetime mortgage is similar to a regular mortgage, but you make no repayments on the advance, which continues to attract interest in the normal way. The mortgage is repaid from the sale proceeds of the property when you die or move into long-term care.

The use of an equity release calculator may be enough to set you off on the road to unlocking some of the wealth tied up in your home.

Tags:

Business,

Equity,

financial planning,

investments,

money,

stock

July 21, 2016

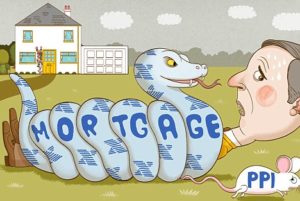

When taking out a personal loan, opening up a credit card or even taking up a mortgage, many often sign a PPI. However reality is that many are usually unaware of this fact, until they are unable to make the needed payments as scheduled. But what is a PP1?

When taking out a personal loan, opening up a credit card or even taking up a mortgage, many often sign a PPI. However reality is that many are usually unaware of this fact, until they are unable to make the needed payments as scheduled. But what is a PP1?

What Is PPI?

Short for payment protection insurance, PPI is normally sold by financial institutions to their customers as a means to protect them in the event they are unable to pay their loans. This is whether the reason behind it is sickness or loss of job. The insurance sometimes goes by the name unemployment coverage, sickness coverage or accident coverage but can broadly be referred to as credit protection insurance.

How to Get PPI money back?

In the event you have coverage and intend on getting your money back as the need has arisen, getting your claim submitted is the first step. This way information regarding just how much PPI has been sold to you on your loan and the amount payable will be revealed. In the end after the necessary paperwork has been completed, you will receive your PPI refund money back.

How much can one claim?

The amount of PPI you can claim largely depends on the amount of loan and credit card balance you have. This simply means the larger the loan and credit card balance, the bigger the PPI refund. However to know the exact amount you will need to make and offer and add the interest to know just how much you are entitled to. Take into account where you have gotten your mortgage from, all places you have taken loans from and credit cards that you have signed up for over the years. This way if you have ever signed up for PPI, the retrieval process will begin.

How far back can you claim?

In this case also there is usually no set limit. With some, register claims can be made as far back as 12 years with many having a maximum of 15 years. However you will only know whether you can get your funds back by making a claim as far back as you can. This way ensure you gather all your paperwork on the accounts you bought PPI.

How Soon Can You get your money back?

There is usually no set limit on how long it will take to return the funds to customers. However on average the time usually takes about 8 weeks. This still depends on the bank, its procedures and your history with the bank.

Filing a claim

The process of making a claim to get a PPI refund is no doubt long and tiring. In this case to make the process easy using iSmart is ideal. With the services being particularly free, you will not be charged to check whether you have a PPI on your loans. In addition no charges will be brought to you in case you chose another company to file a claim, even after knowing how much you can get as refund. Still with some lenders taking as many as 2 months to respond whether your claim can be made or not, leaving it to the professionals is better saving you time and money. As if that is not enough with PPI scandals affecting many people in the past decade, ppirefund.co.uk will ensure that even after your complaint has been rejected, you get the needed advice on what to do next.

Tags:

Business,

Credit Card,

Funds,

insurance,

investments,

money,

mortgage,

Payments

June 23, 2016

Setting up a small business on your own isn’t an easy task. As a one man band you have to learn how to deal with every business function from marketing to IT. One area of your business where it really pays to outsource is in the finance department and hiring a qualified accountant makes a lot of financial sense for most businesses.

Setting up a small business on your own isn’t an easy task. As a one man band you have to learn how to deal with every business function from marketing to IT. One area of your business where it really pays to outsource is in the finance department and hiring a qualified accountant makes a lot of financial sense for most businesses.

Once your business starts to grow though and you begin taking on employees, the temptation is to move more and more of the businesses functions in-house. Whilst this can make sense in some areas, with payroll it really does pay to outsource.

In this article I want to look at four areas where outsourcing the payroll function can save your business a lot of money and time and prevent difficulties further down the road as you expand your workforce.

Resource Savings

Time is money in business and payroll can be very time consuming. As your business expands so too will the time needed to perform the payroll function in-house. Investing in payroll software can also be expensive and keeping it up to date is another drag on your time and resources. Factor into this the training needed to bring staff up to date with the software and any updates and developments and you can begin to see the constant drain on resources that doing your payroll in-house can be.

Staff Recruitment and Absence

One of the clear benefits of outsourcing payroll functionality to an accountancy firm is the stability and consistency it brings to developing expanding businesses. All businesses are vulnerable to the danger of key talent leaving them for sunnier pastures and retaining staff is a core part of HR strategy, especially in the early days. Outsourcing payroll effectively removes the worry of having to recruit and train a new staff member to perform this vital business function on which every employee depends. For smaller businesses, having a single individual in charge of payroll also comes with inherent risks in terms of unplanned absence. Payroll isn’t something that can be put off, so if your payroll administrator is off sick then someone else will need to fill in for them, diverting their precious time away from their core duties.

Compliance

In accounting, accuracy is paramount. The UK’s laws around payroll are strict and any mistakes due to human error can and often do result in fines. Not only is this an unnecessary and unwelcome cost, it also means your payroll administrator has to go back over their work to identify and rectify the error. Accountancy firms deal with payroll every day and have the systems and oversight procedures in place to avoid these kinds of accounting errors. Not only this but HMRC’s rules and regulations are prone to change, meaning re-training your payroll staff. The Real Time Information for PAYE changes introduced in 2013 for example, now means companies have to send a Full Payment Submission to HMRC before every payday as well as a monthly Employer Payment Summary. This can mean 76 online declarations a year. That’s a lot of man hours.

Flexibility and Scalability

Creating a successful business is harder than it’s ever been. Recent research from the Harvard Business Review suggests that the average dying age of a publically listed company is 31 years (down from 55 in 1970). Small businesses have to grow and adapt rapidly if they are to be successful and that means so too do their workforces. Unlike many other business functions, payroll isn’t just desirable but required. The consequences for not paying your staff or getting this wrong can be devastating, with the risk of serious damage to the internal reputation of your company and some fairly irate employees. Outsourcing payroll means you can scale your business quickly without the burden of having to grow your payroll functionality too. Accountancy firms have the staff and the resources to handle your growing payroll needs. For seasonal businesses who take on a lot of additional staff in certain months, this can be a real lifesaver.

Tags:

Business,

economy,

money,

Payroll,

planning

April 30, 2016

So, you’ve done your research. You know a well-balanced investment portfolio should ideally include exposure to bullion. But do you go with gold or silver? Truth be told, there’s no one correct answer to that question – at least not one that’s applicable to every investor. Learn the key differences between gold and silver and base your decision on factors including how long you plan to hold onto your investment, how much you are able to invest and what sort of risk profile you want to adopt. Remember, both metals offer inflationary protection and carry no credit risk, whilst each has taken its turn in the limelight as far as past price performance goes. The canniest of investors are likely to go for a long play investment in both metals. Read on, and find out more.

So, you’ve done your research. You know a well-balanced investment portfolio should ideally include exposure to bullion. But do you go with gold or silver? Truth be told, there’s no one correct answer to that question – at least not one that’s applicable to every investor. Learn the key differences between gold and silver and base your decision on factors including how long you plan to hold onto your investment, how much you are able to invest and what sort of risk profile you want to adopt. Remember, both metals offer inflationary protection and carry no credit risk, whilst each has taken its turn in the limelight as far as past price performance goes. The canniest of investors are likely to go for a long play investment in both metals. Read on, and find out more.

The Case for gold

Gold’s volatility factor is up to 70 percent lower than silver’s. Gold also carries more prestige. This is largely due to its rarity. The yellow metal is 18 times rarer than silver. And new discoveries are on the wane. Production has likewise fallen considerably over the last decade. Meanwhile, central banks are still buying up large quantities of the stuff, which is encouraging. Over the longer term, gold’s price has performed exceedingly well. Also in its favour is gold’s unrivalled status as the accepted alternative to currencies. The yellow metal has been used to store wealth for more than 3,000 years. You simply cannot say this of silver.

The case for silver

Silver has much going for it as a savvy investment choice, though its volatility means it is more speculative than gold. Notably, silver is more widely used in industrial applications. Whatsmore, the industries it’s used in – like, solar power and electronics – are growing. Sterling silver jewellery is still a popular gift idea and many people are indulging in silver jewelry for themselves as well. Silver’s price may be currently weak, yet it is this very weakness forcing producers to scale back operations. These aforementioned factors, at some point, are likely to affect silver’s supply and demand ratio to the point where its price will be pushed up. In addition, analysts concur silver may well offer investors better value than gold, as the gold/silver price ratio is currently further apart than it theoretically should be. Finally, even though VAT must be paid on silver purchases, it remains, of course, much cheaper per ounce than gold to buy. This offers those with even only US$1000 in capital to invest in bullion, an ‘in’ into the market.

To conclude

Silver or gold? Each is likely a good investment choice over the longer term. Yet as you’ve just read, they have their differences. Which is precisely why many advisors would suggest owning both. If you choose a total exposure to bullion amounting to 10 percent of your portfolio for instance, go ahead and split that 10 percent between silver and gold. How you weigh the split largely depends on your views on the health of the stock market and worldwide industrial growth.

Tags:

Assets,

Business,

economy,

gold,

investments,

money,

Silver

March 6, 2016

A well thought out marketing strategy is an important component for every business. One of the things to consider when developing a marketing strategy is figuring out which marketing channels to invest in.

A well thought out marketing strategy is an important component for every business. One of the things to consider when developing a marketing strategy is figuring out which marketing channels to invest in.

There are many different options, but not all of them make sense for every business. It is; therefore, best to invest in the marketing channels that are most appropriate for your target market. The rise of social media and internet usage has made digital marketing platforms extremely relevant. Here are four marketing channels you should be investing in.

Social media

According to EMarketer, there were over 1.43 billion social media users in 2012. This is a 19% increase from the 2011 figures. It’s obvious that social media usage is rapidly expanding, making it the perfect platform for a well-developed marketing strategy.

It is easy to target the right audience through networks like Facebook, which allow for targeted advertising. Twitter is a great way to share small amounts of information about products with a large number of people. There are also other social media networks; like LinkedIn, Tumblr, FourSquare, that can help market products at a fraction of the traditional cost.

Search engine marketing

Ranking high in search engine results is important as only the highest ranked websites get the most traffic. Search engine marketing includes paid advertisements, search engine optimization, and pay-per-click services. Investing in a new website and search engine marketing (SEM) services is not expensive. Most companies that provide SEM services will help develop the website, and website content for an all-inclusive price as well. SEM is a great way to increase the visibility for your product online, and works well with social media marketing methods as well.

Event marketing

Event marketing allows companies to target more specific groups of people as compared to traditional marketing methods like TV advertisements or billboards. It consists of sample distribution, interactive displays, and visual promotions at events. It is very common for companies to sponsor entire events – Mercedes Benz Fashion Week – which are branded to market a specific product.

You can also see event marketing in action at malls, where free samples are being provided. This means that companies – regardless of their marketing budget – can participate in this marketing channel as it is customizable. It is worth the money since it targets a specific type of customer in a more personal way as compared to other marketing channels.

Trade shows

Trade fairs (trade shows) allows companies to promote their products to a large number of potential consumers in the very short space of time. By having trained staff at the booth, collecting leads and quickly following up on them, it can be very easy to turn these potential consumers into actual buyers. This is one of the best methods for creating a lasting impression on consumers.

There are plenty of marketing channels available, but you should focus on using the ones that deliver the most bang for the buck.

Eva has been helping small businesses to improve their promotions for the last 3 years. Her expertise is in custom promotional merchandise, through her work at Custom Gear, one of Australia’s fastest growing branding companies.

Tags:

Business,

Capital,

economy,

investments,

money

Many homeowners have a considerable amount of cash tied up in the equity of their homes – that is, the value of the amount of the home they own, less any outstanding mortgage or loan.

Many homeowners have a considerable amount of cash tied up in the equity of their homes – that is, the value of the amount of the home they own, less any outstanding mortgage or loan.

Recent Comments