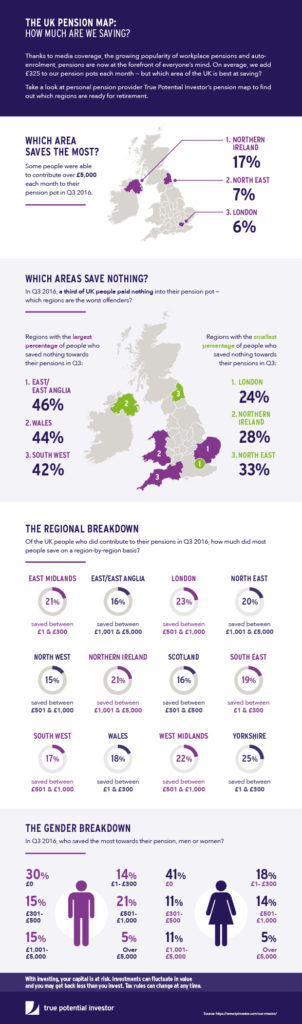

June 1, 2017

On average, we add £325 to our pension pots every month, but which area of the UK is best at saving? Find out more from the infographic below from personal pension provider, True Potential.

Created by online investment service company, True Potential

Tags:

economy,

investments,

money,

Pensions,

personal finance,

Retirement,

Returns

April 16, 2017

The new year and the new presidential administration has ushered in a host of fiscal changes that could impact your wallet. Safeguard your money and act in the best interest of your household or business’s bottom line by learning more about the growing financial trends in 2017.

The new year and the new presidential administration has ushered in a host of fiscal changes that could impact your wallet. Safeguard your money and act in the best interest of your household or business’s bottom line by learning more about the growing financial trends in 2017.

Rising Interest Rates

Interest rates are on the rise in 2017, creating a financial environment that is geared more toward saving than borrowing. In fact, people who put money into personal savings and retirement accounts have the opportunity to create and grow their wealth. Alternatively, people who need to borrow money face paying higher interest rates and making larger payments on their loans each month.

The higher interest rates correlate to the expanding economy and the creation of more openings in the American job market. As unemployment rates go down and American workers may more money, they have the unique opportunity this year to save money and take advantage of rising interest rates that could lead to greater personal wealth. Capital management services offered by professionals like James Dondero are also expected be more in demand this year.

Freelancing in Retirement

This year also has the makings of being the ideal time for retirees to make some extra cash doing side gigs. It is no secret that retirees are living longer and often outliving the money they have set aside for this time in their lives.

Until recently, however, people in this age demographic had few chances to earn extra cash. Many employers did not want to invest time and effort into training employees who would leave the workforce sooner rather than later.

However, thanks to companies like Uber and Lyft that rely on freelancers, senior citizens now have the opportunity to work for themselves as independent contractors and earn money that will not put their Social Security incomes in jeopardy. Along with driving for Uber or Lyft, they also can freelance as writers, artists, tutors, and other independent contractors.

Investment Portfolio Automation

This year also shows signs of increasing the demands for investment portfolio automation. This automation makes investing with financial pros like James Dondero easier and essentially creates an ideal if not passive way for people to put money into the stock market without putting forth any unnecessary effort on their part.

Further, this automation shows promise of being tax efficient and low in cost. Moreover, it costs the same if not less than an exchange-traded fund.

About James Dondero

James Dondero began his career in the financial industry in 1984 and has since become one of the leaders in capital and investment management. As the co-founder and president of Highland Capital Management, L.P. in Dallas, Texas, Dondero also serves as the CEO and chairman of the board at HCM Acquisition Company. Before founding Highland Capital Management, L.P. he worked for top financial companies like American Express and Protective Life.

He graduated with top academic honors from the University of Virginia’s McIntire School of Commerce with dual degrees in finance and accounting. He is certified as a Certified Management Accountant as well as a Chartered Financial Analyst. He also volunteers for Dallas-based charities and organizations like the George W. Bush Presidential Library and Institute, Education is Freedom, Snowball Express, and the Perot Museum of Natural Science.

Tags:

Business,

economy,

financial planning,

investments,

money,

Retirement

August 16, 2014

Retirement planning is a serious business and the sooner you get into it, the better. We often tend to procrastinate, thinking that we have enough time left for the same, but this often makes the task tougher than it would otherwise have been. So the question is what exactly is retirement planning, and how important is it for your future?

Retirement planning is a serious business and the sooner you get into it, the better. We often tend to procrastinate, thinking that we have enough time left for the same, but this often makes the task tougher than it would otherwise have been. So the question is what exactly is retirement planning, and how important is it for your future?

The process of retirement planning involves determining what kind of funds should be available to you at the time of retirement, to live comfortably post your retirement. There are a lot of factors that you would need to consider like when will you want to retire, where will you live, and what kind of a lifestyle will you have post retirement. Each additional year you want to retire early raises your goal considerably as you need to account for all the regular monthly expenses, medical and emergency expenses, vacations, celebrations etc.

When you see the costs add up after keeping in mind the inflation, this is likely to be your retirement goal and is clearly dependent on the type of life that you wish to lead. You may come across many typical figures that people throw at you regarding a retirement corpus that one should have, for example 20 times your income and so forth, which can be only used as some vague guideline. You must consider some important points to make sure that you are a smart investor when it comes to your retirement investing.

Evaluate the available instruments for retirement savings

There is a host of saving options available in the market when you want to invest for your post retirement days. There are many tax- efficient ways that can help you build up your retiral kitty, some of which can be availed directly through the employers while other plans are available through investment brokers or banks. However, it is important to closely look at each of these options to determine the benefits and derive the maximum profit by using them judiciously, when your aim happens to be a healthy retirement corpus.

There are some good retirement options that you can explore at your employers, as some may offer unmatched benefits and even give some kind of cushioning against the volatile stock market conditions. It is important to understand and evaluate the risk and benefits associated with each of the options. It is often seen that younger investors are more bent on investment options that have higher returns even if they have higher risks as they have enough time available to recover from the losses that may arise. However, in case you do not have too many years before you retire, then it’s best to avoid such options as you may not be able to recover if you lose your investments and will be better off with some conservative instruments with lower risk factors.

The following are some of the options available for planning your retirement:

- 401 (K) and other Employer Plans: There are several employer driven plans like the 401(K)s that can be utilized by the individuals to build up their retirement kitty while saving a considerable amount of tax too in many cases. They are also quite hassle-free as you can directly get the amount debited from your paycheck.

- Fixed Benefit Plans: There are many employer sponsored plans that offer a fixed the sum of money based on certain factors like salary drawn and the years of service one has put in at the establishment .

- IRAs or the Individual Retirement Accounts: These allow you to move pretax amounts up to certain annual limits towards tax efficient investments. These investments can also be tax deferred.

- Roth IRA: This can be seen as a retirement option that is similar to a traditional IRA though there are certain differences in the taxation of the contributions as well as the distribution income.

- SEP IRA: This is targeted at the employer or self-employed individuals, and they can direct 100% of their contributions towards various channels of their choice.

- SIMPLE IRA: this is a commonly used retirement plan by employers with 100 or less employees in that establishment.

Tags:

401K,

budgeting,

financial planning,

Financial Retirement,

investments,

money,

Retirement,

Retirement Planning

January 23, 2014

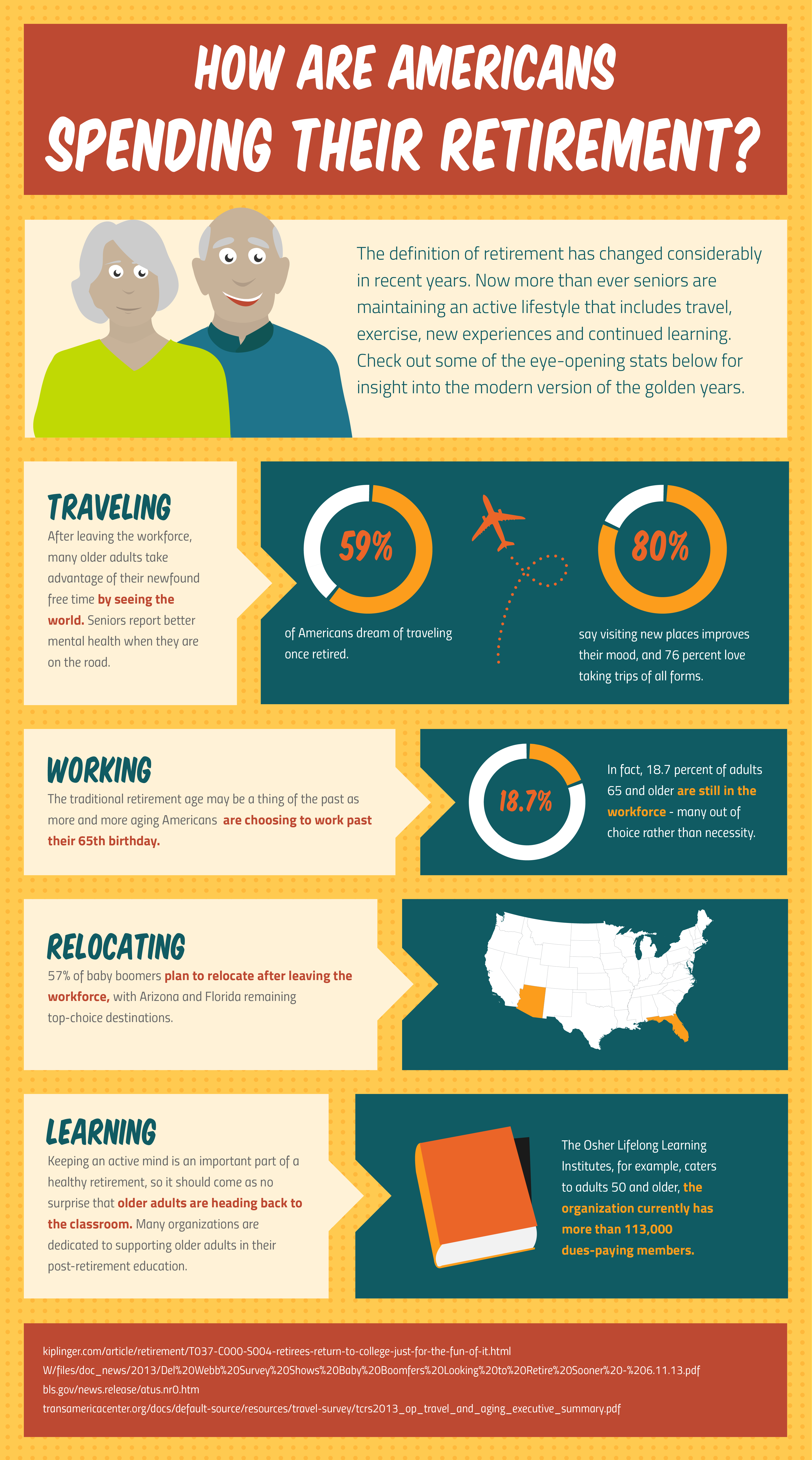

The commonly held perception of retirement living is rapidly changing. No longer are older adults settling down after leaving the workforce. Today’s retirees are more focused on active living, whether in the form of exercise, volunteering or picking up a new skill. These new trends will certainly have an impact on the financial strategies of the nearly 10,000 baby boomers turning 65 each day. Here’s a look at how the latest generation of retirees plan on spending their golden years.

Tags:

budgeting,

Interest Rates,

money,

Retirement,

Retirement Savings,

savings

May 31, 2012

Are you reaching that point in your life when you have to plan for your retirement? You must not rely on your social security money alone for covering all the expenses after your retirement. Not having a proper retirement plan will lead to a bad situation after your retirement and that is something that you must avoid. Here are 4 retirement plans that you can consider and choose from.

Are you reaching that point in your life when you have to plan for your retirement? You must not rely on your social security money alone for covering all the expenses after your retirement. Not having a proper retirement plan will lead to a bad situation after your retirement and that is something that you must avoid. Here are 4 retirement plans that you can consider and choose from.

1. The 401(K) Plan

This is one of the most popular plans that employers use to secure their employee’s retirement. According to this plan, you must match your employer’s contribution to the plan (which oscillates between 1% and 6% of the payment) to take full advantage of the plan. Plan your investment properly so that you can take full advantage of it after retirement. Failing to match your employer’s contribution will make the investment in this retirement plan redundant. There are many other flexible investment plans for helping you with your contribution to the retirement plan. Choose one that you can afford.

2. Savings Incentive Match Plan for Employees (SIMPLE) IRA

Many small time employers secure their employee’s retirement using this plan instead of the 401(K) plan. The only difference between these two plans is the fact that this plan has no maintenance fee as such from the employer’s side and thus is a popular choice with most small time employers. The contribution that the employee is supposed to make to this plan is deducted automatically from the pay check.

3. Traditional IRA (Individual Plan)

It is always advised that you should maintain an individual retirement plan along with the employer’s retirement plan that is already in place. The contribution that you can make to this plan is limitless and depends on your personal financial abilities completely. The contribution eligibility is set at $5,000, plus $1,000 catch up for those over 50 years old, but not per account.

4. Roth IRA (Individual Plan)

This plan is similar to the Traditional IRA plan with the same limit and eligibility criterions. The only difference is the fact that the contributions you will make to this plan is not income tax deductible.

In case you find out that you are ineligible for the IRA individual plans, you can always set up an annuity fund. The tax benefits are lower than the tax benefits one gets with the IRA funds and also the contribution fees are higher than usual. These shouldn’t deter you from having a solid retirement plan in the first place.

Tags:

cash,

economy,

financial planning,

Golden Years,

money,

Retirement,

Retirement Planning,

savings

Recent Comments